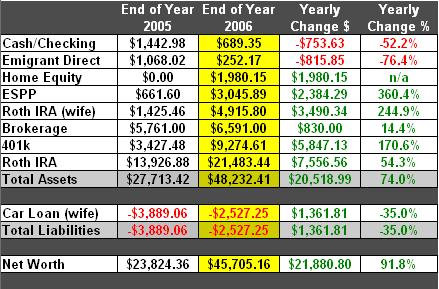

2006 was a good year for us. We purchased our first home, my wife is a year closer to graduation, and our net worth nearly doubled from $23, 824 to $45,705. I wont complain about a 91.8% increase. Here’s a closer look at each account:

Cash/Checking: This tends to go up and down a fair amount each month. We use it for our regular expenses and make sure the credit cards are paid off each month, so we aren’t trying to increase this total.

Emigrant Direct: This account was holding the money we were saving for our down payment, so it grew until it got emptied when we purchased our home. In the past, I’ve discussed Emergency Funds ( Do You Need an Emergency Fund?) and I still feel largely the same way, but that being said, we would like to increase this account to $1,000 as a small emergency fund, just in case… This will be one of our first priorities in 2007.

Home Equity: As I’ve mentioned before, I wasn’t sure whether or not I wanted to include home equity in our net worth calculation. In the end, I decided to for various reasons including the fact that we plan to sell it within the next 10 years. That being said, I am being very conservative with the amount I assign. It does not include the amount we paid as a down payment nor does it take into account any appreciation in the value of our home. It is more like the amount of the mortgage that has been paid off.

ESPP: I receive a 15% discount when my company stock is purchased, and it has performed well. Although I don’t want to be overly weighted in company stock, I wouldn’t mind increasing my contributions here.

Roth IRA (wife): My wife is not the financial junkie that I am, but she does like seeing the gains in her Roth IRA, and anything that gets her more interested in our finances is a good thing.

Brokerage: I haven’t added any money to this account for a couple of years. It was the first investment account I opened, before I knew much about investing and before I had better options like a 401k and ESPP. It has continued to make decent gains, so for now I will keep the money there until I find a better investment opportunity for that money.

401k: This is starting to grow into a decent amount. I actually lowered the percentage that a contribute to my 401k when we purchased our home, and while I am still above the amount required for the maximum company match, I would like to increase my contribution percentage back to where it was.

Roth IRA: I’ve maxed out my Roth IRA every year since I’ve had it and I plan to do more of the same in the future.

Car Loan: My wife has been making the regular monthly payments all along. The interest rate is low, so it hasn’t been a priority to get it paid off. Now, with some things out of the way, as soon as we have $1,000 in our Emigrant Direct account, we will focus on getting rid of this loan. I am sick of subtracting its total from our asset’s total.

We’ve got high expectations for what we can accomplish in the upcoming year. Thank you all for your support, and let’s all have a prosperous 2007!

Let’s see…if you can pull off a 92% increase next year you’ll have 87.75k in the bank, do it again you’ll have 168k, and in 5 years would have $1.2 Million. How beautiful would that be?

Joe,

That sounds pretty good to me. I’ll see if I can make that happen. :)